Older workers are staying on the job longer, in part to counter lackluster performance of retirement accounts and housing values. Meanwhile, the high unemployment rates of Generation X and Millennials could help explain the rise of young adults living with their parents.

Long-Term Trend

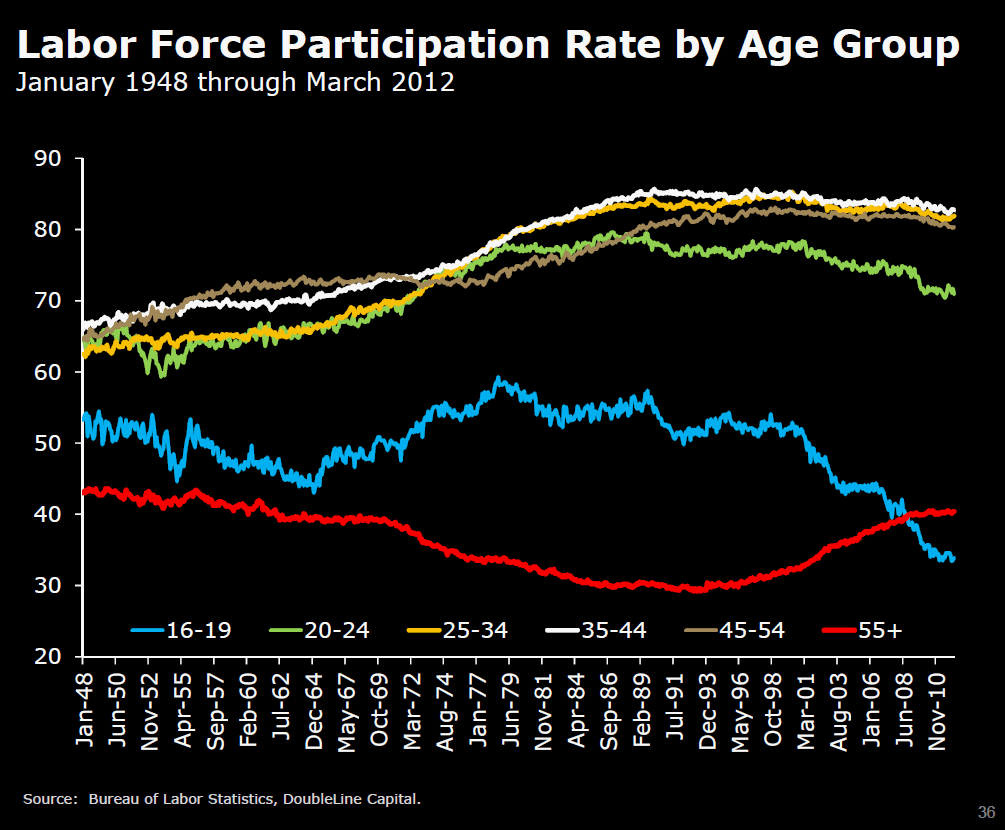

The trend of falling employment as a share of the 54-and-under population and rising employment among those 55 and up has been in force for more than a decade.

See this chart for the labor participation rates going back to 1948.

Walter Russell Mead on the politics of this generational job divide

Related articles

- Are Baby Boomers Stealing Jobs from the Young? (Part 1) (businessinsider.com)

{kind=link}